Category II AIF: The Structural Advantage Most Investors Overlook

For sophisticated investors seeking long-term value creation in India's unlisted space, the Category II AIF structure offers a combination of flexibility, tax efficiency, and governance that no other vehicle matches.

The Investor's Dilemma

India offers no shortage of investment vehicles. You can invest in mutual funds, Portfolio Management Services (PMS), hedge funds structured as Category III AIFs, or venture capital through Category I AIFs. Each has a place. But for a specific type of investor — one seeking high-conviction, long-duration bets on India's growth story with proper governance and tax efficiency — none of these is ideal.

This is where the Category II Alternative Investment Fund (AIF) earns its structural advantage. It is the vehicle of choice for private equity, private credit, and distressed asset funds that need to operate with institutional discipline.

Understanding the Landscape

Before examining Category II specifically, it helps to compare the vehicles side by side:

| Vehicle | Min. Investment | Universe | Taxation | Liquidity |

|---|---|---|---|---|

| Mutual Fund | ₹500–5,000 | Listed only | Investor-level | High (open-ended) |

| PMS | ₹50 Lakhs | Listed only | Direct liability | Moderate |

| Cat I AIF (VC) | ₹1 Crore | Startups / early-stage | Pass-through | Very low (7–10 years) |

| Cat II AIF | ₹1 Crore | Listed + Unlisted, Debt, Structured | Pass-through | 3–5 year horizon |

| Cat III AIF | ₹1 Crore | Listed + derivatives | Fund-level MAT | Variable |

The Three Core Advantages

1. Investment Universe Flexibility

Category II AIFs can invest across the full spectrum:

- Listed equities — flexible mandates (long-only or concentrated)

- Unlisted equities — early stage, growth stage, pre-IPO

- Structured products — convertible notes, compulsorily convertible debentures (CCDs), preference shares

- Debt instruments — high-yield credit, mezzanine financing

This breadth is critical for a consumption-focused fund. The most interesting opportunities in India's consumption story are not always listed. The mid-market SME generating ₹100 crore in revenue with 30% EBITDA margins and a clear pathway to ₹400 crore — that company does not yet exist on any exchange. A Category II AIF can own it, nurture it, and harvest the value when it lists.

2. Pass-Through Taxation: The Hidden Alpha

This is perhaps the most significant structural advantage, yet the most misunderstood.

In a Category III AIF (hedge fund) or a private limited company structure, the fund itself pays tax at the maximum marginal rate (often 25-40% including surcharges) before distributing profits. This creates a "tax drag" that compounds negatively over time.

Category II AIFs are pass-through entities. The fund itself does not pay tax on investment income (other than business income, which is rare for investment funds). Income and capital gains flow through directly to investors, who are taxed at their applicable rates.

A Hypothetical Example:

Consider a ₹100 gain on an investment.

-

Structure without Pass-Through:

- Fund Profit: ₹100

- Tax at Fund Level (say 30%): -₹30

- Distributable Surplus: ₹70

- Result: ₹30 of capital is lost to tax before it even reaches you.

-

Category II AIF (Pass-Through):

- Fund Profit: ₹100

- Tax at Fund Level: ₹0

- Distribution to Investor: ₹100

- Result: You receive the full ₹100. You pay tax based on the nature of the gain (e.g., 12.5% for Long Term Capital Gains on unlisted shares, or slab rates for interest), allowing for far better tax planning and compounding.

"Pass-through tax treatment means every rupee of realized gain flows directly to the investor's account. Over a 5-year period, this tax efficiency can add 200-300 basis points to your net IRR."

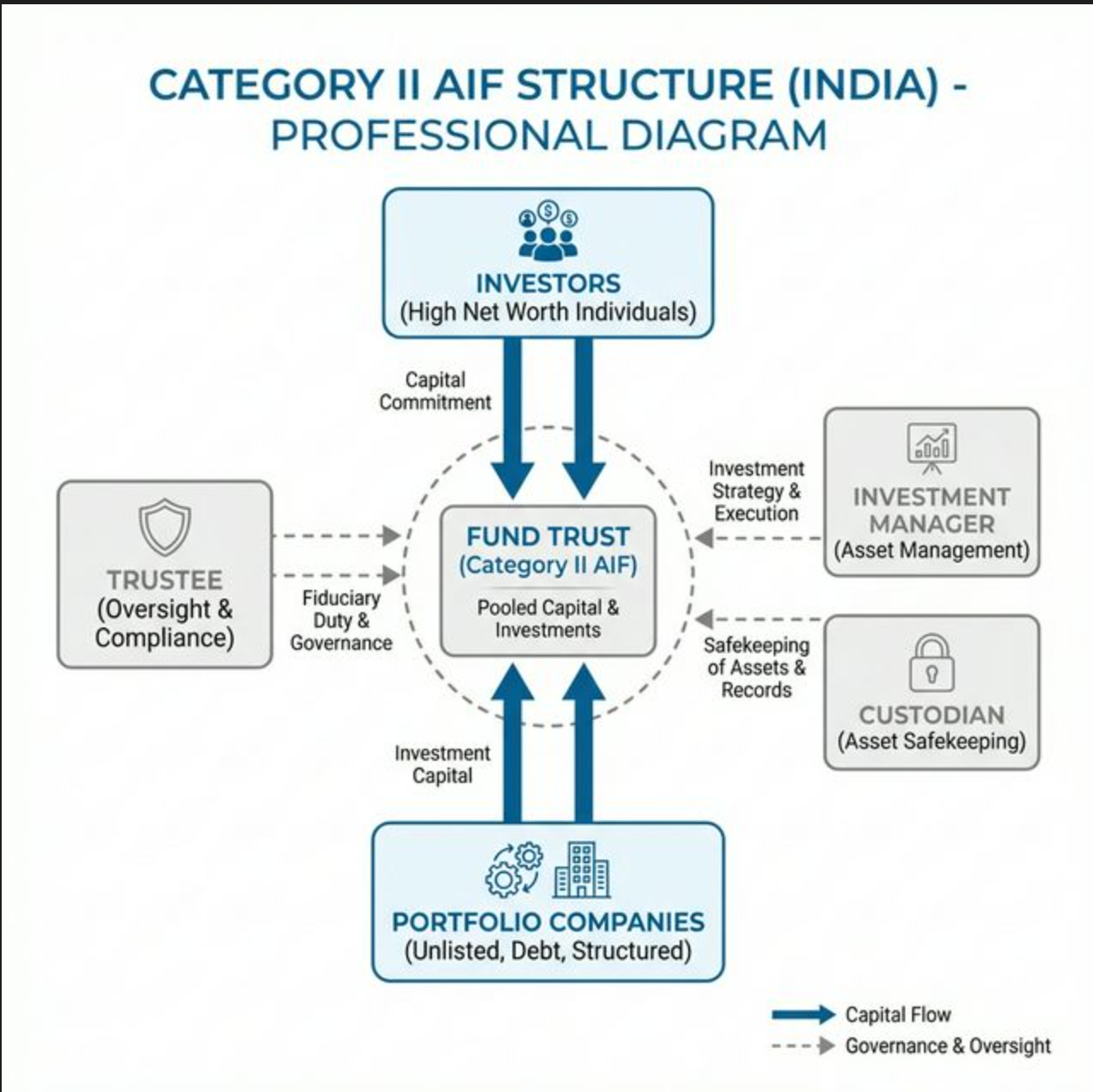

3. Governance and Safety

Category II AIFs operate under SEBI's AIF Regulations, which mandate a rigorous separation of powers:

- Independent Trustee: Holds the assets in trust for the beneficiaries (you). The investment manager cannot touch these assets directly.

- Custodian: A regulated entity (like a bank) that executes all settlements.

- Statutory Audit: Mandatory annual audits and valuation by registered valuers.

- Concentration Limits: SEBI mandates diversification (e.g., max 25% in one company), preventing "all-in" bets that risk capital preservation.

This governance architecture is far more robust than a PMS, where the manager has significantly more discretionary authority with fewer structural checks.

Patient Capital: The "J-Curve" Advantage

Category II AIFs are close-ended structures, typically with a 3–5 year investment period and a defined exit horizon. Many investors initially view lock-in as a disadvantage. In reality, it is a feature that protects returns.

The best consumption investments in India require patient capital.

- Year 1-2 (Sowing): Capital is deployed to scale operations, build brands, or expand distribution. Financials might look flat or dip as expenses rise (the "J-curve" dip).

- Year 3-4 (Growing): The investments yield results. Revenue compounds, margins expand due to operating leverage.

- Year 5 (Harvesting): Exit via IPO, strategic sale, or secondary sale at a premium valuation.

Liquid vehicles (mutual funds) often face redemption pressure during market downturns, forcing managers to sell their best stocks at the worst times. A Category II AIF manager is immune to this short-termism. They can hold through volatility and exit only when the value is maximized.

Who Should Consider a Category II AIF?

The Category II AIF structure is designed for Ultra HNIs, family offices, and institutional investors who:

- Have a minimum investment horizon of 3–5 years.

- Seek exposure to India's unlisted consumption and mid-market opportunity.

- Want institutional governance with pass-through tax treatment.

- Are looking for a differentiated return stream, uncorrelated with listed markets.

The ₹1 crore minimum investment reflects this positioning — it is not a mass-market product. It is a sophisticated vehicle for sophisticated investors.

Conclusion

The Category II AIF structure is not just a regulatory category. It is a deliberate architecture optimized for long-term compounding.

By combining the flexibility to invest in high-growth unlisted winners, the efficiency of pass-through taxation, and the discipline of SEBI-regulated governance, it offers a superior risk-adjusted path for participating in India's consumption story.

This article is for informational purposes only. Prospective investors should consult their tax and legal advisors before making investment decisions. Category II AIF investments carry risk of loss of capital and are suitable only for eligible investors as defined under SEBI AIF Regulations.

More from PriQuant Insights

Capital Is Leverage, Not a Product

Top managers don't "manage money." They deploy optionality. Here's the operating system behind how serious capital gets wielded — and the mental models that separate capital wielders from capital managers.

Read →The Profitable Blind Spot: Why SME Mid-Market Is India's Most Overlooked Investment Opportunity

While venture capital chases unicorns and large PE writes ₹500 crore cheques, a vast middle ground of profitable, cash-generative Indian businesses sits starved of institutional capital. This is where we invest.

Read →India's $3,000 Inflection Point: Why Now Is the Moment for Consumption Investing

When a country's GDP per capita crosses the $3,000 threshold, history shows consumption doesn't just grow — it accelerates exponentially. India is crossing that line right now.

Read →